Work in Progress

Abstract

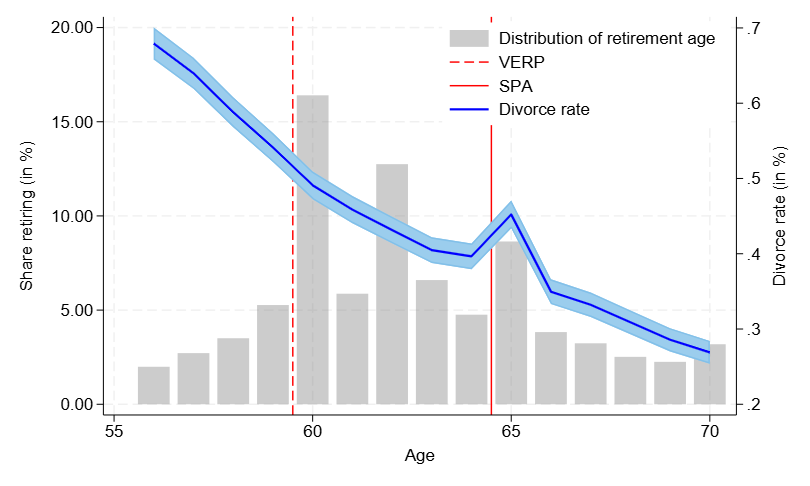

Social insurance programs often make benefits a function of household size, to account for economies of scale in consumption of couples. Due to endogeneity problems, empirical estimates of responses to such policy design are sparse. This paper aims to fill the gap by exploiting variation around exogenous age thresholds in a state pension with this feature. In response to a near-universal change in incentives to living alone, we estimate an increase in the share living alone of 0.2% pt (0.8%). This is driven by a permanent 5% fall in new cohabitation starts and a one-off 20% spike in the risk of separation and divorce. The findings are robust to controlling for kinks in mortality, timing of actual retirement, and we find little evidence of fraud.

Abstract

There is large variation across countries in whether pension wealth is divided or treated as separate property in divorce. This paper is the first to study the effects of these policies on divorce decisions, labour supply and late-life outcomes. Using administrative data from a country that treats pension wealth as separate property, we show that divorce is associated with delayed retirement for women. We then build a dynamic structural model of household bargaining, divorce and retirement and simulate the effects of counterfactual pension division policies. Compared to the no-compensation default, introducing pension splitting at divorce significantly decreases the retirement age for divorced women, with small or negligible effects for divorced men and married couples. For a given level of transfer, the labour supply effect is much stronger for women compared to men, as they value the pension wealth more due differences in life expectancy. When state pension benefits are means-tested against other income, there is a small total increase in state pension payments, because labour supply responses outweigh the effect of a mechanical reduction in pension wealth inequality.

Abstract

Accurately modelling interdependence of labour supply decisions of individuals living with a partner is crucial for understanding women’s labour market participation. For this purpose, I describe how a recently proposed generalisation of two-agent models that covers the whole spectrum from non-cooperation to perfect cooperation can be used to study couples’ labour supply and housework division. Whilst generally increasing levels of caring raises individual and household utility, this is not the case when caring is very asymmetric. Furthermore, in this model a rise in the wage of the lower earner decreases utility of the higher earner due to the effects on within-household distribution of consumption. This is not the case for household productivity: all else equal, the partner who is less productive in the household has higher utility. And, lastly, whilst labour supply elasticities increase with within-household wage inequality, they do so at a higher rate for couples with high cooperation and vice versa.